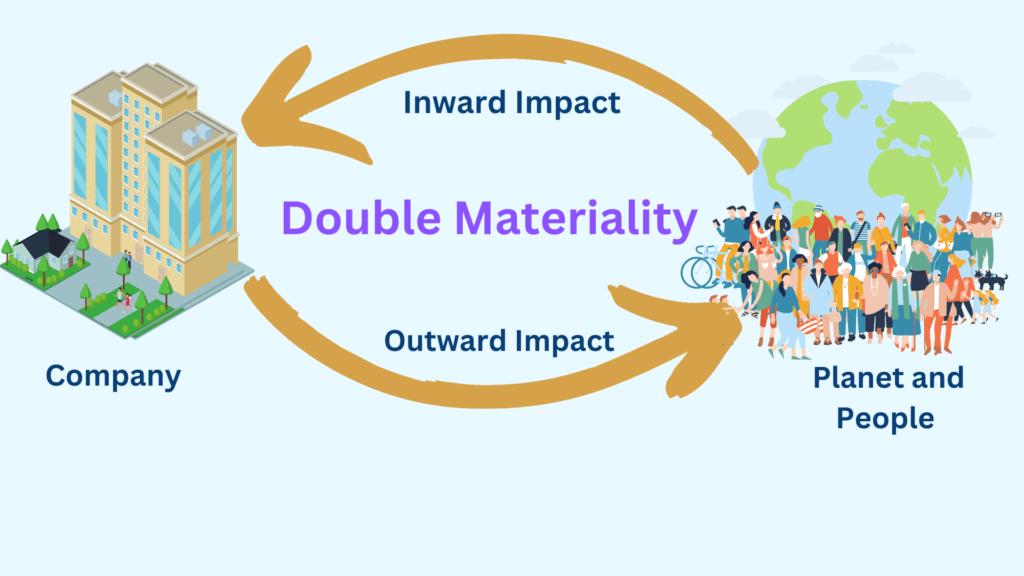

The concept of double materiality underscores the essential relationship between an organization’s internal operations and its broader external surroundings, emphasizing both perspectives as significant. In essence, this comprehensive evaluation not only looks at an organization’s environmental and social impact but also the potential impacts of external factors on the organization itself. This dual perspective reflects the very essence of the double materiality concept and underpins the Corporate Sustainability Reporting Directive (CSRD) mandate.

Corporate Sustainability Reporting Directive (CSRD) and Double Materiality

CSRD is an innovative framework focused on transparency and accountability in sustainability reporting. One of its fundamental components is the double materiality assessment, which goes beyond financial performance and internal operations. It obliges organizations to evaluate their societal and environmental impacts, shaping an understanding of the risks and opportunities in their value chain.

Understanding Double Materiality Assessment

The essence of Double Materiality Assessment (DMA) is embedded within the CSRD, which requires businesses to identify, assess, and report on sustainability matters that significantly affect their performance or the environment and society. This approach ensures that companies consider both the impact of sustainability risks and opportunities on their operations and the effect of their activities on the environment and society.

DMA distinguishes two dimensions:

1. Outside-In Materiality: This refers to the external risks and opportunities arising from environmental, social, and governance (ESG) factors that might impact the financial performance and position of the company.

2. Inside-Out Materiality: This reflects the impact of the company’s business activities on the environment and society, which in turn may have reputational, legal, or market implications.

The identification of material ESG factors from both perspectives allows companies to comprehensively understand and manage their sustainability risks and opportunities.

The Role of Double Materiality Assessment in CSRD

Environmental, Social, and Governance (ESG) factors are at the heart of sustainability reporting, providing the basis for impact materiality assessment. This concept of double materiality, embodied in the CSRD framework, ensures that these ESG factors are fully integrated into the reporting process. It empowers organizations to appreciate the full scope of their activities’ impacts on people and the environment while recognizing potential risks or opportunities for their financial performance.

Under CSRD, companies are required to conduct a Double Materiality Assessment to identify and report on material sustainability matters. This twin perspective helps companies identify risks and opportunities linked to sustainability that could affect their financial performance (outside-in) and the impacts of their business operations on the environment and society (inside-out).

In essence, the DMA allows businesses to gain a comprehensive overview of their sustainability footprint. This can help them improve their risk management strategies, enhance their business resilience, and position themselves more favorably in a market increasingly focused on sustainable and socially responsible practices.

The Scope of CSRD and Double Materiality in Reporting

CSRD expands the scope of sustainability reporting, reinforcing the importance of materiality assessments. Central to this is the double materiality concept, which requires companies to report their impacts on society and the environment and their business’s impact from these external factors. As a result, organizations need to consider material topics from two perspectives: impact materiality and financial materiality. This dual evaluation provides a holistic view of the organization’s most significant impact, which, combined with understanding the supply chain, helps address sustainability matters that are material from both a financial and an impact perspective. In the context of the CSRD, this approach not only meets regulatory requirements but also meets stakeholder demands for corporate transparency.

An organization’s senior management and experts need to come together for a robust double materiality assessment. This holistic approach will help organizations not only identify entity-specific sustainability matters but also how their products and services contribute to or mitigate sustainability risks and opportunities in the short, medium, or longer term. The assessment will also help understand what is happening in the value chain, leading to an increasing need for certain parts of the organization to be involved in sustainability matters.

Implications of Double Materiality Assessment for Companies

The introduction of the CSRD and its DMA requirement holds several implications for companies. First, it requires a significant level of organizational readiness to identify, assess, and disclose material sustainability matters. Businesses must develop robust systems for gathering and analyzing relevant data, and they must cultivate a deep understanding of ESG issues.

Secondly, the DMA will influence how businesses strategize and make decisions. By revealing potential sustainability risks and opportunities, the DMA can inform strategic planning, operational decisions, and risk management processes. It can also help businesses anticipate and respond to stakeholder expectations, regulatory changes, and market trends.

Finally, the DMA’s transparency requirement means that companies will face increased scrutiny from investors, regulators, and the public. This could, however, be a boon for businesses that excel at managing and reporting on their sustainability impacts, as they may be able to attract socially conscious investors and customers, and potentially gain a competitive advantage.

Stakeholder Engagement and the Double Materiality Assessment

A fundamental part of the double materiality assessment is the active engagement of stakeholders, essential in the process of identifying sustainability matters of material importance. Furthermore, it supports organizations in understanding their value chain’s impact materiality and financial materiality, giving a complete picture of risks and opportunities from both internal and external perspectives. Through such stakeholder engagement, organizations can better identify their most significant impacts on society and the environment, resulting in more comprehensive and accurate sustainability reporting standards.

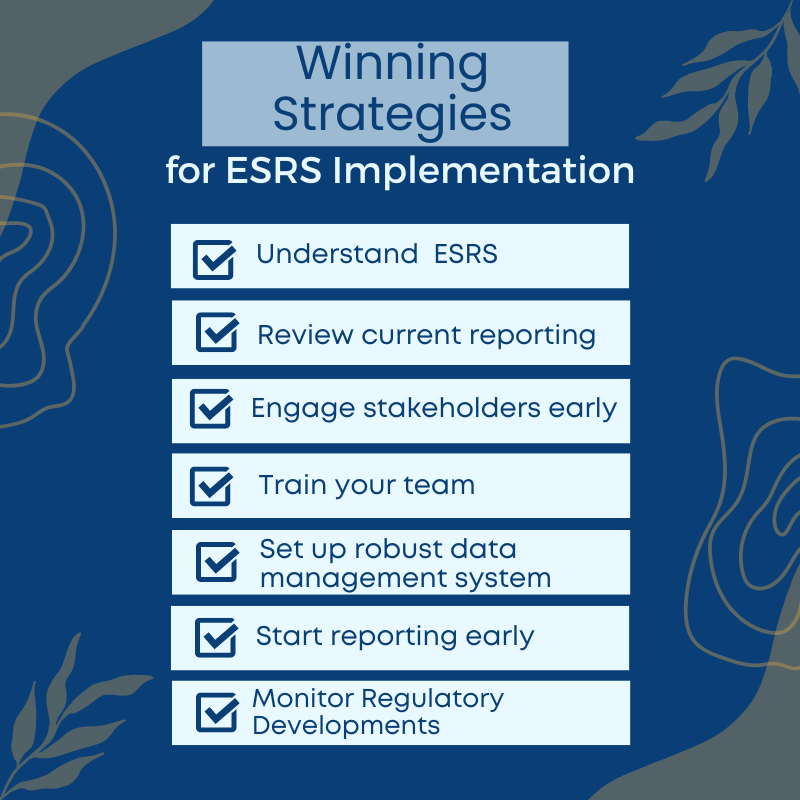

Strategies for Effective DMA under CSRD

Implementing a successful DMA under the CSRD requires strategic planning and a multi-disciplinary approach. Companies may consider the following steps:

1. Establish a Cross-functional Team: A team with diverse expertise – including risk management, sustainability, finance, and corporate communications – will be better equipped to conduct a comprehensive DMA.

2. Leverage Existing Frameworks: Companies will employ guidelines and requirements in the European Sustainability Reporting Standards, namely the ESRS 1: General Requirements, Chapter 3. Additionally, companies can draw on established sustainability reporting frameworks like GRI and SASB to help identify and assess material ESG issues.

3. Engage Stakeholders: By consulting with stakeholders, businesses can gain insights into the ESG issues that are most relevant to their operations and most important to their stakeholders.

4. Develop Robust Data Management Systems: Effective DMA requires accurate, reliable data. Developing robust systems for collecting, managing, and analyzing ESG data will be essential.

5. Communicate Effectively: Clear, honest, and accessible communication about the results of the DMA will be crucial for maintaining stakeholder trust and meeting the CSRD’s transparency requirements.

Conclusion

The CSRD and its DMA requirement represent a significant evolution in corporate sustainability practices. By identifying and managing sustainability risks and opportunities, companies can not only comply with the directive but also enhance their business resilience and competitiveness in an increasingly sustainable world. The journey to effective DMA under CSRD may be challenging, but with strategic planning and stakeholder engagement, businesses can navigate it successfully.

📣 Break Free from the Shackles of CSRD & ESRS Compliance

🔎 Do you find yourself tangled in the complex web of CSRD and ESRS regulations? Seek no more!

🧐 With our custom-tailored solutions, CSRD and ESRS compliance is no longer a grueling challenge. We offer a streamlined, efficient process designed to fully leverage your resources. Moreover, our solutions have been meticulously crafted to meet and exceed stakeholder expectations. In this increasingly competitive landscape, our innovative compliance strategies give you the edge to outshine your competitors.

💖 Imagine a world where meeting regulatory deadlines isn’t synonymous with stress! With our timely, smooth compliance solutions, you can finally beat the clock without breaking a sweat. Imagine the tranquility of a seamless CSRD compliance transition – that’s not just a dream, it’s our promise.

💼 Don’t let the complexities of CSRD and ESRS compliance be your stumbling block. Choose our all-inclusive solutions for a stress-free compliance journey. Start now and embark on a path of smooth transitions and peace of mind. Leave the stress behind, and let us guide your journey to effortless CSRD compliance.